Americans for Earned Wage Access

Responsible Earned Wage Access (EWA) shifts the power of payroll to consumers

Utilized by millions, EWA empowers and protects consumers by creating an important alternative to high-cost loans

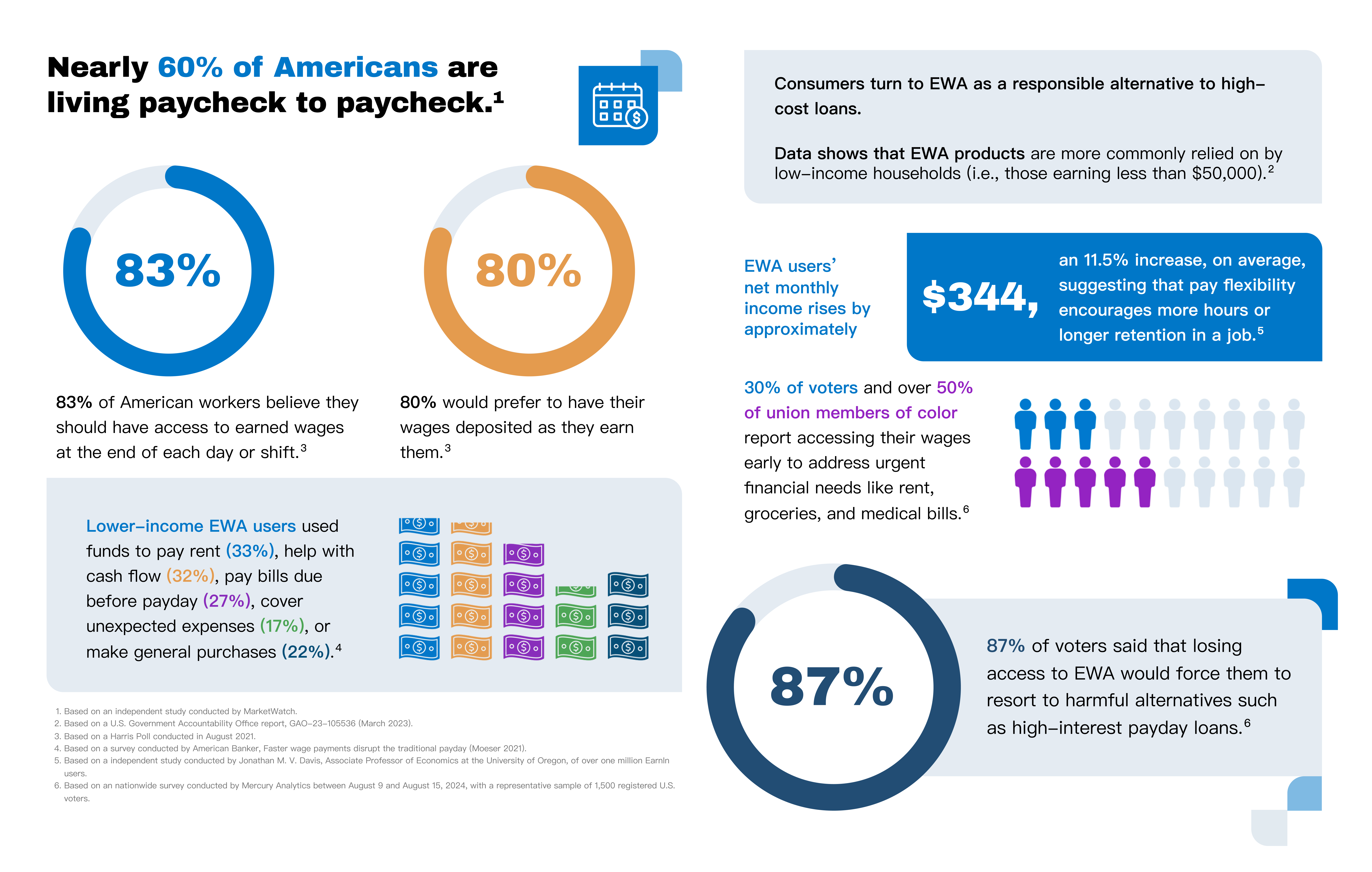

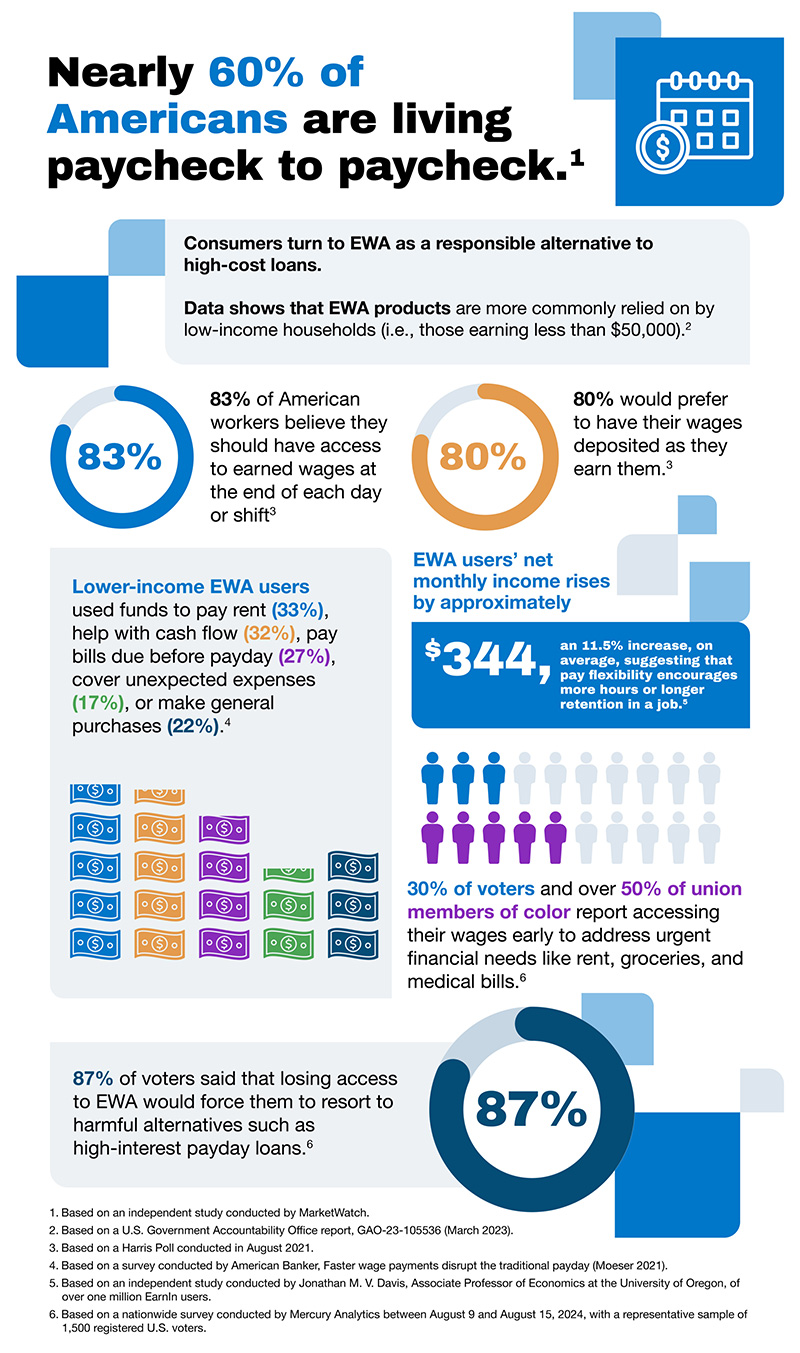

EWA enables workers to access wages they’ve already earned before an arbitrary payday to manage short-term financial needs and smooth income distributions. Responsible EWA products are already used by millions of Americans, giving them greater control over their earned income to manage daily and unexpected expenses without creating debt. EWA offers a safe, convenient, and responsible alternative to predatory loans and other high-risk, high-cost products.

Research from the Financial Health Network found that the vast majority of users have a positive experience with EWA and said that continued, responsible use improves their ability to pay bills on time.

An industry advocating for regulation – and clear, consistent consumer protections

A clear, tailored regulatory framework that recognizes the unique structure of EWA will protect consumers through strong safeguards while preserving responsible innovation and consumer choice. EWA providers seek a robust regulatory framework that ensures responsible providers will continue to operate.

EWA is not a loan or credit, and should not be regulated as such. It is non-recourse, with no interest, no late fees, and no credit checks. Attempting to fit EWA oversight into existing regulatory structures or misclassify it as a loan would jeopardize access to a vital and financially empowering tool used by millions of Americans and push consumers—especially income-constrained consumers—toward high-risk alternatives.

Why Americans Need EWA

U.S. workers agree: We need EWA

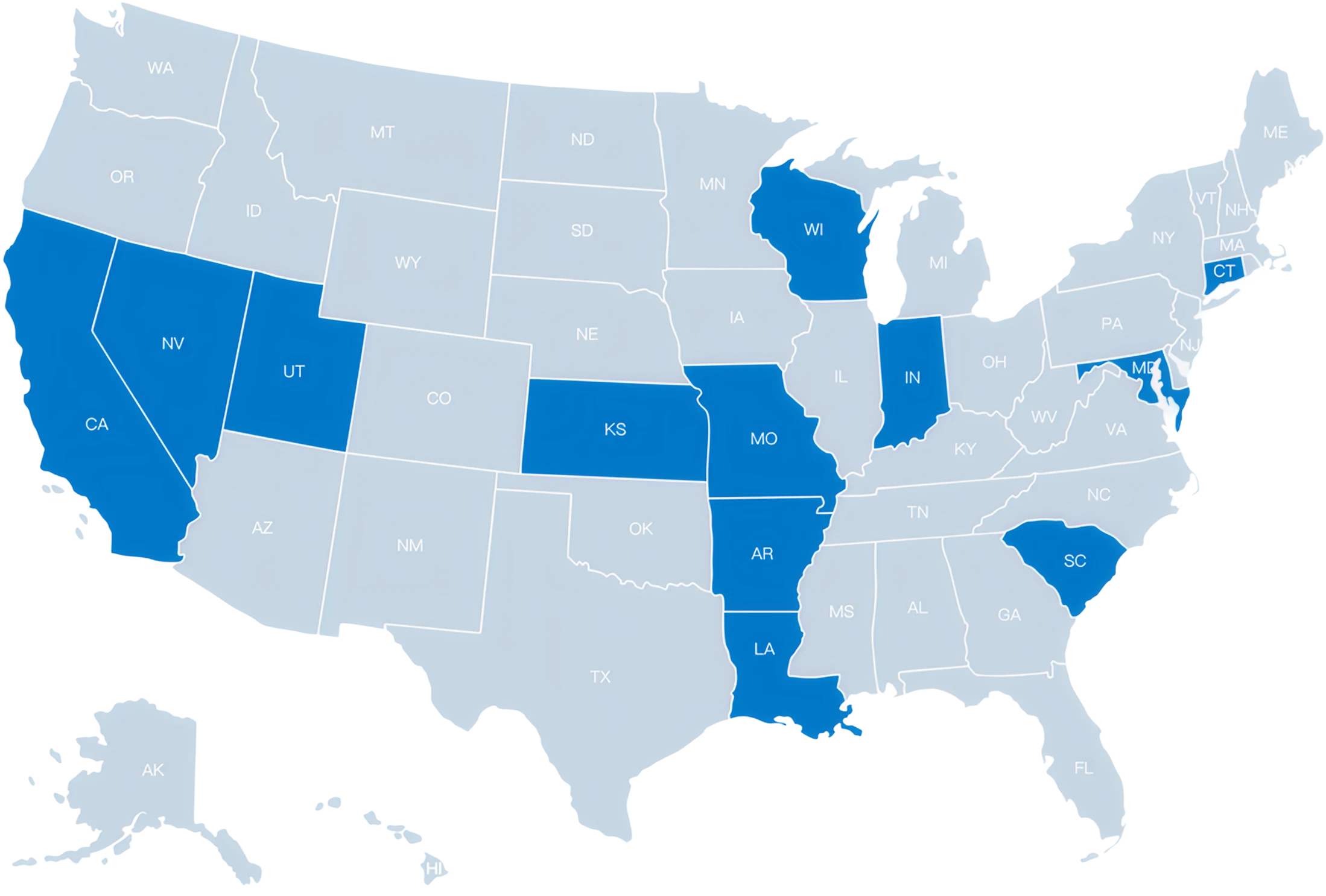

The current state landscape

As an emerging financial product, EWA doesn’t fit into traditional lending laws. EWA is properly classified as a unique financial service distinct from loans in 12 states, but state-by-state regulatory frameworks without tailored federal oversight risk creating a patchwork of policies limiting the availability of EWA products based on residence.

The current federal landscape

Rep. Bryan Steil’s has released a bipartisan discussion draft of the Earned Wage Access Consumer Protection Act. This draft legislation represents another important step toward long-overdue regulatory clarity for earned wage access. By establishing a national consumer protection framework and reinforcing that EWA is not a loan, this proposal recognizes the core principles of responsible EWA products and avoids forcing them into outdated lending laws that simply don’t fit.

Establishing a bespoke federal framework through Congressional action that recognizes EWA as a product distinct from loans and credit is critical to preventing misclassification that would eliminate safe options and push consumers toward high-risk alternatives. The CFPB’s new Advisory Opinion accurately defining and explicitly clarifying the core principles of EWA is a constructive first step, and provides the perfect opportunity to codify strong industry rules.

Congress is looking at this issue right now, and American workers need clarity. Federal lawmakers must ensure Americans continue to have access to safe and transparent EWA services.

.png)

.png)

.png)

%20Logo_Color_png.png)

.avif)

.webp)